When 'Covered' Isn't: How Insurance Denials Quietly Become Your Personal Debt Crisis

Most people sign their insurance paperwork believing they have purchased a form of financial protection. They pay premiums faithfully, carry their cards in their wallets, and proceed through medical appointments or property repairs with the reasonable assumption that coverage will perform as advertised. Then a denial notice arrives, and the machinery of personal debt quietly begins to turn.

What follows that single letter—often dismissed as bureaucratic noise or a clerical error—can cascade into one of the most damaging financial events a household encounters. Collection accounts, credit score deterioration, wage garnishment, and years of repayment pressure are not hypothetical outcomes. For millions of Americans annually, they are the direct and foreseeable consequence of an insurance claim that was rejected and never formally challenged.

Understanding why this happens, how quickly it happens, and what can realistically be done to stop it is not a matter of financial sophistication. It is a matter of financial survival.

The Gap Between What You Think You Owe and What Providers Say You Owe

When an insurer denies a claim, the financial obligation does not simply evaporate. Hospitals, specialty clinics, restoration contractors, and other service providers have already rendered services. They require payment. In the absence of an insurer honoring its commitment, the provider's billing department turns its attention to the individual policyholder.

This is the moment most people misunderstand. Many assume that a dispute with their insurer protects them from immediate billing pressure. It generally does not. Providers and insurers operate on separate contractual tracks. A patient or homeowner may be actively appealing a denial while simultaneously receiving escalating bills from the provider—bills that, if unpaid beyond a certain threshold, move into collections regardless of the appeal's status.

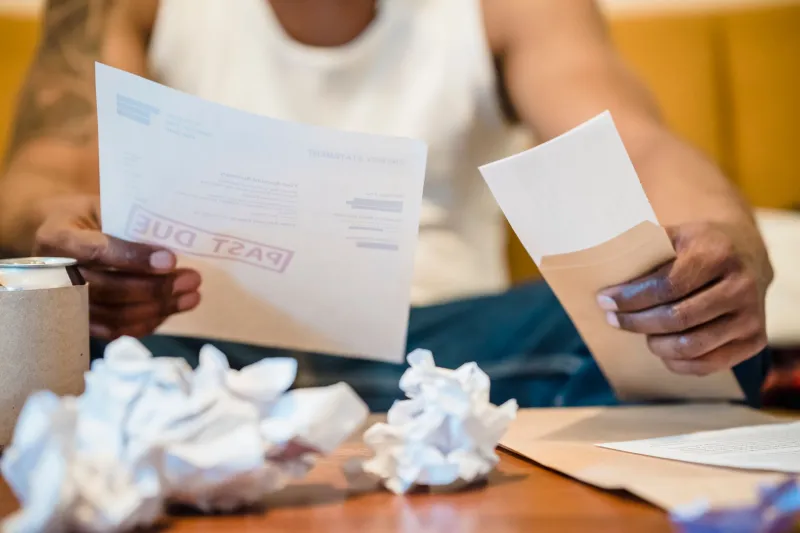

The timeline is often shorter than people expect. Many medical providers begin the collections referral process within 90 to 180 days of an unpaid balance. Property damage contractors may move faster. A denial notice received in January can, without intervention, produce a collections account by summer—an account that will remain on a credit report for up to seven years.

Why the Appeals Process Goes Unused

Federal law, specifically the Affordable Care Act and the Employee Retirement Income Security Act for employer-sponsored plans, grants insured individuals the right to appeal denied claims. Most state insurance commissioners maintain additional consumer protection frameworks. The appeals infrastructure exists. The problem is that most people do not use it.

Several factors contribute to this gap. Denial letters are frequently written in dense, technical language that obscures both the reason for denial and the path forward. Deadlines for internal appeals—typically between 30 and 180 days depending on the plan and the nature of the denial—are easy to miss when a household is managing the stress of an illness, property damage, or financial anxiety. And many Americans simply assume that if their insurer said no, the answer is final.

It is not. Internal appeals overturn denials at a meaningful rate. When internal appeals fail, external review—conducted by an independent organization—is available under federal law for most plans and results in policyholder victories in a substantial portion of cases. Yet according to available research, fewer than one in ten people who receive a denial ever file a formal appeal. The financial consequences of that inaction are borne entirely by the individual.

Practical Steps Before a Denial Becomes a Debt

The window between receiving a denial notice and sustaining lasting financial damage is finite but real. Taking structured action within that window is the single most effective intervention available to policyholders.

Request the explanation of benefits immediately. An Explanation of Benefits, or EOB, is the document that details exactly why a claim was denied. Insurers are required to provide one. The specific denial code listed on the EOB determines the most effective grounds for appeal—whether the issue is a coding error, a prior authorization failure, a determination of medical necessity, or a network classification dispute.

Contact the provider's billing department directly. Explaining that a denial is under appeal and requesting a hold on collections referral is not guaranteed to succeed, but many providers will grant a temporary pause when a policyholder demonstrates active engagement. Document every conversation, including the name of the representative and the date.

File the internal appeal in writing. Verbal complaints carry no formal weight. A written appeal, submitted within the plan's deadline and accompanied by supporting documentation—physician letters, medical records, comparable coverage precedents—creates a paper trail that protects the policyholder and strengthens any subsequent external review request.

Invoke external review if the internal appeal fails. Under the ACA, most health plans must offer access to an independent external review organization. The external reviewer's decision is binding on the insurer. This step costs nothing for the consumer and removes the conflict of interest inherent in having an insurer review its own denial.

Engage your state insurance commissioner. Filing a complaint with the state insurance regulatory authority serves two purposes: it creates an official record and, in many cases, prompts the insurer to reconsider the denial in order to avoid regulatory scrutiny.

When the Debt Has Already Formed

For households that have already passed through the denial-to-collections pipeline, the situation is serious but not irreparable. Collections accounts related to insurance disputes carry a distinctive characteristic: they are frequently disputable under the Fair Debt Collection Practices Act if the underlying liability was improperly transferred from insurer to consumer.

Consumers have the right to request debt validation in writing within 30 days of first contact from a collections agency. If the debt cannot be validated—or if the original denial is overturned on appeal even after collections activity has begun—the account may be removable from credit reporting.

For medical debt specifically, recent changes to credit reporting standards have reduced the impact of certain medical collections on credit scores, and the Consumer Financial Protection Bureau has proposed further restrictions. These developments do not eliminate the problem, but they provide additional leverage during negotiation.

The Structural Issue Beneath the Paperwork

Insurance denials do not occur in a vacuum. They are, in part, a product of a system in which the financial incentives of insurers and the financial security of policyholders are not fully aligned. Claims review processes, prior authorization requirements, and network adequacy standards all function as friction points where coverage obligations can be narrowed or redirected.

Policyholders who understand this dynamic are better positioned to respond to it. Reading a policy before a crisis occurs, understanding what prior authorization is required, knowing which providers are in-network, and maintaining records of all insurer communications are not bureaucratic inconveniences. They are the foundational practices that determine whether a denial notice remains a dispute or becomes a debt.

The financial time bomb embedded in a denial letter does not detonate automatically. It detonates when no one defuses it. The appeals process, imperfect and demanding as it is, remains the most reliable mechanism available to American households for preventing an insurer's decision from permanently altering their financial trajectory.